John Lewis

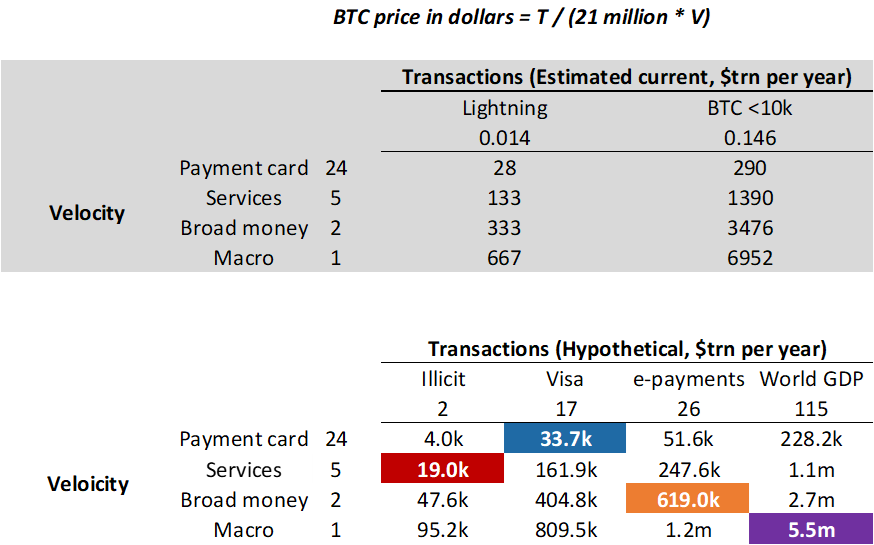

The recent near halving of Bitcoin’s price has reignited debate about its true value. As a store of value, net present value asset pricing models suggest it should be worth zero because it pays no dividend. Yet its price remains far above zero, and its total value is still large despite recent turbulence. In this post I explore the question: what’s Bitcoin’s value as a means of exchange? I show that using a simple quantity theory of money framework helps explain its extreme volatility, the powerful influence of sentiment, how prices can surge even when transaction usage is low, and – crucially – why innovations by competitors and limited retail payment adoption pose significant downside price risks.