Abstract

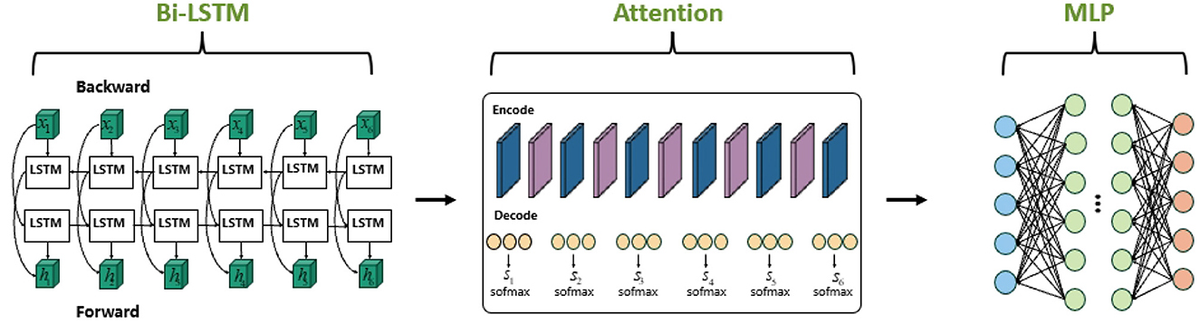

Stock price prediction plays a crucial role in investment, corporate strategic planning, and government policy formulation. However, stock price prediction remains a challenging issue. To tackle this issue, we propose a novel hybrid model, termed M-A-BiLSTM, which integrates Attention mechanisms, Multi-Layer Perceptron (MLP), and Bidirectional Long Short-Term Memory (Bi-LSTM). This model is designed to enhance feature selection capabilities and capture nonlinear patterns in financial time series. Evaluated on stock datasets from Apple, ExxonMobil, Tesla, and Snapchat, our model outperforms existing deep learning methods, achieving a 15.91% reduction in Mean Squared Error (MSE) for Tesla and a 5.95% increase in R-squared (R2) for…