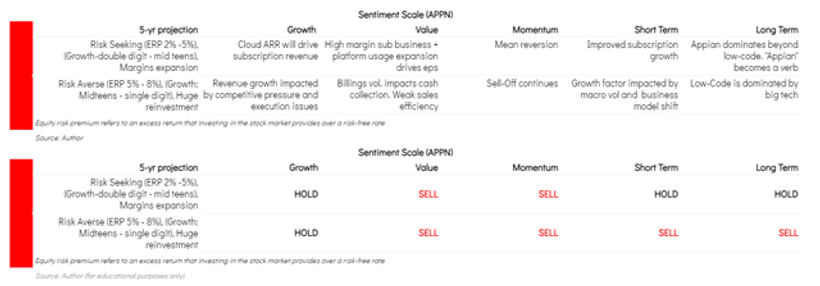

For Appian (APPN), the case for buying the recent dip is weak. The modest growth outlook, declining profitability, weak momentum, and frothy valuation relative to peers make it tough to project a near-term rebound. I am projecting more mean revision in the near term. In the long term, Appian needs to keep investing in its platform to pull away from competitors as it remains tough to pick a winner in the low-code space.

Demand (Bullish)

Low Code-BPO-Digital Transformation-RPA

My bullish rating…